“Practical men who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist. Madmen in authority, who hear voices in the air, are distilling their frenzy from some academic scribbler of a few years back.” – John Maynard Keynes

Modern Monetary Theory (MMT) is the latest craze to hit left-wing circles; the supposed panacea to the problems that a future Bernie Sanders administration or Jeremy Corbyn government will likely face.

Advocated by leading lights of the Democratic Party in the USA, such as Alexandria Ocasio-Cortez (AOC), and by those trying to gain the ear of Jeremy Corbyn and John McDonnell in the UK, MMT is currently the talk of the town on the left. And it’s not hard to see why. After all, the concept offers activists an easy rebuttal to right-wing critics who ask how radical policies will be paid for.

In this sense, MMT might as easily stand for ‘magic money tree’. That, after all, is what this theory promises: a way of funding everything we want, and more, without having to worry about the hassle of taxation or – more importantly – class struggle.

Think the left’s shopping list of demands are unaffordable? Think again! Want free healthcare and education? No problem, we’ll just print money. Mass investment in green energy? Don’t worry, we can turn on the government’s taps. Build a million council homes? Easy – we’ve got MMT.

But, truth be told, Modern Monetary Theory is a bit of a misnomer. In reality, it is not much of a theory. Nor is it particularly modern. As John Maynard Keynes once noted, those imagining themselves to be ‘pragmatic’ and ‘practical’ are all too often in fact the slaves of some defunct economist – in this case, none other than Keynes himself.

Consensus breaks

The fact that a broad debate has opened up around economic alternatives to austerity should come as no surprise to anybody. After a decade of crisis and cuts, workers and youth are rightly calling into question the neoliberal consensus that has continued to hold court, despite the seemingly never-ending ‘Great Recession’.

The fact that a broad debate has opened up around economic alternatives to austerity should come as no surprise to anybody. After a decade of crisis and cuts, workers and youth are rightly calling into question the neoliberal consensus that has continued to hold court, despite the seemingly never-ending ‘Great Recession’.

With growth stalling, business investment stagnant, and monetary policy at its limits, even mainstream capitalist economists (generally of a Keynesian variety) are now challenging the demand for balanced budgets. After all, with austerity failing and interest rates at 0%, what other weapons do governments have left in their arsenal?

For the bourgeois priesthood that defends this capitalist creed, however, any criticism of the all-powerful ‘invisible hand’ of the market is sacrosanct. Hence the barrage of attacks and insults that is thrown in the direction of any alternatives put forward.

“MMT is appropriate only in exceptional situations,” claimed John Llewellyn, a former chief economist of the OECD, “where economies are far from full employment, deflationary pressures are in evidence, and interest rates are at the zero bound”.

The problem for Llewellyn and his cohort, however, is that these “exceptional” conditions are the ‘new normal’. The situation he describes sounds very much like that which the world economy has faced for the past decade or more.

Larry Summers, an economic advisor to Barack Obama and former head of the US Treasury under Bill Clinton, has even described the global economy as being in a state of “secular stagnation”: one with permanently subdued demand and muted private investment, where “fairly ordinary growth” is sustained only by “extraordinary policy and financial conditions”.

This situation, Summers argues, has existed not just since the 2008 crash, but in the decades preceding it also. The world’s economic engine has only been kept going thanks to an endless injection of cheap credit and government stimulus. The ‘exception’, then, has become the rule.

Those criticising MMT from the right, therefore, clearly aren’t in a very strong position to do so. After all, as Paul Krugman, the Nobel Prize winning economist, admitted in a speech to an audience at the London School of Economics in the wake of the 2008 crash: “Most work in macroeconomics in the past 30 years has been useless at best and harmful at worst.”

Unfortunately for the MMTers, however, two wrongs do not make a right. And it is the duty of socialists to provide an honest appraisal of the ideas being proposed, in order to show the way forward for the labour movement.

What is MMT?

First off, it should be noted that MMT is a tricky beast to define. Indeed, this eclectic theory has almost as many versions as there are followers.

First off, it should be noted that MMT is a tricky beast to define. Indeed, this eclectic theory has almost as many versions as there are followers.

Of interest to us here, however, are those who put forward MMT from a supposedly left perspective. These include, amongst others: Stephanie Kelton, a senior economic adviser to Bernie Sanders; Bill Mitchell, a vocal MMT advocate who has managed to gain an audience with left-wing MPs in Britain; and Richard Murphy, a prominent tax campaigner and political economist in the UK.

In order to deflect criticism, MMT’s devoted army of followers attempt to bamboozle their opponents with a series of contortions and mental gymnastics. Traditional economic ideas are turned inside out and upside down, confusing the viewer like the optical illusions of an Escher painting. As the Economist journal wryly noted:

“Speaking with MMT’s adherents is sometimes like watching a football match with friends who insist the ball remains stationary while every other element in the game, including the pitch and goalposts, moves around it.”

In fact, even MMT’s own supporters state that it is less a theory, and more a “description of how the monetary system works”; an analytical “lens” that can help us to see the existing economic reality.

Putting aside the fact that a theory, in a scientific sense, is precisely an analytical explanation of reality, what is it then that MMT has to offer? What supposedly radical new perspective does this “massive paradigm shift” provide?

Most fundamentally, MMT asserts that:

- A government that issues its own sovereign, ‘independent’ currency can never run out of money, since it can always choose to pay for any debts by creating more money.

- Inflation will not kick in if such a government spends lavishly and runs a budget deficit, as long as there is spare productive capacity in the economy.

- Taxes do not fund public spending. Governments, therefore, do not need to tax first in order to spend later. Indeed, the real process at play (we are told) is the opposite – governments spend on goods and services, and then adjust tax rates in order to manage demand in the economy.

Although this ‘description’ of the economy doesn’t explicitly lead to any policy conclusions, MMT has unsurprisingly been leapt upon by some left-wingers for what it necessarily implies: that governments need not worry about balancing the books, and can always find the money to foot any bills.

Indeed, this has been spelt out by leading MMT proponents. For example, when rhetorically asking her followers on Twitter “Can we afford a Green New Deal?”, Stephanie Kelton replies: “Yes. The federal government can afford to buy whatever is for sale in its own currency.”

Q: Can we afford a #GreenNewDeal?

A: Yes. The federal government can afford to buy whatever is for sale in its own currency.— Stephanie Kelton (@StephanieKelton) February 7, 2019

Elsewhere, Richard Murphy, has stated that: “What this [MMT] means is that there is no requirement per se to balance the government’s books. Indeed it is not just illogical but completely economically perverse to seek to do.”

Despite being the self-proclaimed author of ‘Corbynomics’ and founder of demands such as ‘People’s Quantitative Easing’ and the UK’s version of the Green New Deal, Murphy has been kept at arm’s length by the Labour leadership, who have categorically rejected MMT and its policy prescriptions.

What is money?

At root, the problems with MMT lie with its (mis)understanding of what money is, and what role money plays under capitalism.

At root, the problems with MMT lie with its (mis)understanding of what money is, and what role money plays under capitalism.

MMTers subscribe to a theory of money known as ‘chartalism’. This term was coined (no pun intended) by a German economist called Georg Friedrich Knapp, who put forward a hypothesis called ‘the state theory of money’.

In short, Knapp asserted that money originates with the state and its imposition of taxes upon a people. The state, according to chartalists, creates money – and then creates a demand for this particular currency by insisting on its use as a ‘means of payment’.

To truly understand the nature of money, however, we must turn to another 19th century German economist: Karl Marx.

In Capital, Marx noted that “the riddle presented by money is but the riddle presented by commodities”. In other words, to understand the role of money in society, we must first understand its real origins – those of commodity production and exchange.

Marx explained that money’s history is tied to the rise of the commodity: goods and services produced not for individual consumption, but for exchange. All commodities, Marx showed, have an exchange value. This is a relationship – a ratio – between commodities, expressing how much of one product would (on average) be exchanged for another.

Building on the ideas of his predecessors, such as David Ricardo, Marx outlined how the value of a commodity is dependent on the labour embodied within it. This labour consists both of the ‘dead labour’ contained within the raw materials, tools, etc. required for its production, and the ‘living labour’ labour added in the production process by the worker.

Marx called this total labour the ‘socially necessary labour time’: the time required for the production of a given commodity, based on the current level of technology and industry, etc. within society.

With this in mind, Marx explained in his Contribution to the Critique of Political Economy how money serves several functions:

- As a unit of account, or measure of value. In money terms, this is represented by prices.

- As a medium of exchange. In this role, money breaks up the circulation of commodities into two separate acts: an act of sale (C-M, a commodity exchanged for money); and an act of purchase (M-C, money exchanged for a different commodity).

- As a store of value, allowing accumulated wealth to be maintained and preserved over time.

- And as a means of payment, allowing debts (denominated in a certain currency) to be settled and taxes to be paid.

Money, therefore, plays a number of roles. Above all though, money is a representation of value: the ultimate expression of the generalisation of the law of value; the logical conclusion of the development of commodity production and exchange, which requires a universal yardstick – a standard measure – against which the value of all other commodities can be expressed.

And yet chartalism (and also MMT) offers no analysis of value, or of commodity production and exchange. As a result, it misses the essence of capitalism, and of money’s role within it.

Money arises historically, not by design, but as a result of the development of commodity production and exchange. It begins primarily as a ‘money commodity’, such as the precious metals, with a value of its own, but later develops to be a mere symbol of value. This is clear today, where money is predominantly not coins, but cash and credit; notes and numbers.

Importantly, in this respect, Marx emphasised that we must understand money as a social relation. Money itself is not wealth, but is a claim to a portion of the total social wealth created in production – ultimately by the labour of the working class.

Money and the state

The chartalists and MMTers, then, are correct to say that the state can create money. But the state cannot guarantee that this money has any value. Without a productive economy behind it, money is meaningless.

The chartalists and MMTers, then, are correct to say that the state can create money. But the state cannot guarantee that this money has any value. Without a productive economy behind it, money is meaningless.

Money is only a representation of value. And real value is created in production, as a result of the application of socially necessary labour time. The money that a state creates, therefore, will only be of any worth in so far as it reflects the value that is in circulation in the economy, in the form of the production and exchange of commodities.

As Marx noted, the sum of the values in circulation must ultimately equal the sum of the prices of these commodities. Where this is not the case, then this is a recipe for inflation and instability.

The state can of course choose what unit of measurement to use when accounting for the value in its economy, just as Americans choose to measure distances in feet, whilst Europeans choose metres. But whether we choose feet or metres, this does not alter the objectives heights of objects in the real world. Nor does constructing more rulers and tape measures.

Similarly, a society does not get wealthier by imagining itself to be so, by printing money or otherwise. As David Graeber explains in his book Debt: the first 5,000 years, referring to the arguments of 17th century English philosopher John Locke and his theories on money:

“Locke insisted that one can no more make a small piece of silver by relabelling it a ‘shilling’ than one can make a short man taller by declaring there are now 15 inches in a foot.”

In any case, Knapp and his MMT followers are wrong to say that the state creates the demand for money. Under capitalism, as the Positive Money campaign have highlighted, the vast bulk of money in circulation – 97% of all money in the economy – is not created by governments but by private banks, in the form of bank deposits.

This money is created in response to demands from consumers and investors, as credit and loans. Where this demand dries up, in terms of falling household consumption and/or business investment, so too does the demand for money.

So the state can create money. But it cannot ensure that this money is put to use. Indeed, the vast programmes of Quantitative Easing that have been conducted across the advanced capitalist world since the 2008 crash are a testament to this.

Trillions have been pumped into the economy by central banks over the past decade, and to what effect? Business investment and GDP growth remain subdued. And yet asset prices – on the stock market and of property, gold, cryptocurrencies, and even artwork and fine wines – froth and fizz like a newly opened bottle of champagne. In short, the speculators are having a field day, whilst ordinary people struggle to make ends meet.

In summary, it is not the state that creates the demand for money, but the needs of capitalist production. And this production is ultimately driven by profit. Businesses invest, produce, and sell in order to make a profit. Where the capitalists cannot make a profit, they will not produce. It is as simple as that.

And yet chartalism – and thus MMT also – has nothing to say about profit, the motor force of the capitalist system. As a result, it cannot explain the real dynamics of the economy under capitalism.

No independence under capitalism

At best, it seems, the ‘revolutionary’ tenets of MMT are just tautological, self-evident truisms. At worst, they are a regurgitation of incorrect ideas that have been proven wrong in practice.

At best, it seems, the ‘revolutionary’ tenets of MMT are just tautological, self-evident truisms. At worst, they are a regurgitation of incorrect ideas that have been proven wrong in practice.

Take the first point outlined earlier, for example, which is the key principle of MMT: governments that run their own ‘independent’ fiat currency cannot go bankrupt.

On one level this is true. A government in a country such as the USA or UK – where the currency is not pegged, and where the central bank can increase the money supply – can always choose to print money to meet its debt obligations or fund a budget deficit.

But firstly, we must ask, where in the world is a government and its currency that is truly ‘independent’ and ‘sovereign’? The whole of the eurozone goes straight out of the window, since it is the ECB [European Central Bank] that calls the tune.

Similarly with the ex-colonial (‘developing’ / ‘emerging’) countries, which are entangled in debts to the big imperialist powers – debts that are for the most part denominated in US dollars. Clearly no ‘sovereignty’ there, either.

And even in a country such as the UK, monetary independence is illusory. Yes, the Bank of England can set interest rates, print money, and lend to the government in its own currency – pounds sterling. But were a radical left-wing government to come in and abuse this power by running large deficits, fuelled by loose monetary policy, in order to carry out large-scale public programmes, this would quickly shake the confidence of the markets.

Within the confines of capitalism, this would lead to an economic catastrophe. The rich would move their money out of the country; the capitalists would carry out a strike of capital; and the government would be forced to hike up interest rates in order to attract investors. The currency would quickly be deemed worthless, leading to rampant inflation – inflation that would hit workers hardest as real wages became eroded by rising prices.

This is no mere conjecture. It is an historical fact. In 1976, the Labour government of the day was faced with precisely this predicament.

Harold Wilson’s Labour had come to power in 1974 in the midst of a world crisis of capitalism, with the economy in a state of stagflation (simultaneous economic slump and high inflation) as a result of decades of failed Keynesian policies. Wilson’s calls for cuts were shouted down by the Labour left, forcing the Prime Minister to resign.

Wilson was replaced by James Callaghan. Worried by a run on the pound, the new PM was forced to go cap-in-hand to the IMF [International Monetary Fund] and ask for a bailout of $3.9 billion – the largest loan ever requested from the IMF at the time.

Needless to say, the Fund’s loan came with strings attached. And so, having won the ‘74 election on a promise to nationalise the top 25 monopolies, Labour found itself instead carrying out austerity, under the diktats of the IMF.

The same could take place today, even in a country like the USA. At the end of the day, the dollar’s ability to act as a world currency arises from America’s relatively hegemonic imperialist position. This, in turn, is derived from the strength and stability of US capitalism.

Only for this reason is the dollar deemed ‘as good as gold’ by international investors. If the US’ ‘strong and stable’ economy was to be called into question by the financial markets, then the dollar too could quickly fall.

“The dollar’s dominance is not guaranteed to last indefinitely,” the Economist recently remarked, commenting on the apparent strength of the dollar in relation to calls for greater government spending.

“When the pound sterling lost its pre-eminence in the early 1930s,” the liberal journal notes, “Britain, with a debt-to-gdp ratio in excess of 150%, faced a currency crisis”. And there is no reason why history could not repeat itself regarding US capitalism and the dollar.

In short, there is can be no such thing as economic, financial, or monetary ‘independence’ for any country within capitalism. Capitalism today is a truly global system, based on a thoroughly-integrated world market and the domination of the major imperialist powers and the multinational monopolies that they protect.

Only by breaking with this system – through the socialist transformation of society internationally – can we be truly independent and free to carry out the economic policies that society needs.

No free lunch

Even if we accept MMT’s claim that certain countries are monetarily ‘independent’ and free to print money, does this really mean that there is no financial barrier standing in the way of a left-wing government?

Even if we accept MMT’s claim that certain countries are monetarily ‘independent’ and free to print money, does this really mean that there is no financial barrier standing in the way of a left-wing government?

The MMTers themselves correctly highlight that there is a limit to any government’s ability to create and spend money – a limit beyond which there will be ramifications in the form of inflation. This limit is the productive capacity of the economy: the economic resources available to a country in terms of its industry, infrastructure, education, population, and so on.

If government spending pushes demand above that which can be supplied, then market forces will push up prices across the board – that is, it will generate inflation. All true so far.

If this point is reached, MMT advocates continue, then it is the job of government to stop the economy from ‘overheating’ by reducing demand. This, they claim, is the role of taxes – to suck money (created by government) back out of the economy, like the control rods in a nuclear reactor, which absorb neutrons and prevent a runaway chain reaction.

But governments do not simply create money and then tax to control demand. Money can be created ‘out of thin air’, but value and demand cannot. Value is produced in production, and this is then redistributed by taxes. And effective demand, under capitalism, is determined by the profitability of production and the limits of the market.

There is no such thing as a free lunch when it comes to capitalism. Whilst the state can print money, it cannot print teachers and schools, doctors and hospitals, or engineers and factories.

Of course, if these things are not being provided and produced by the private sector, then the government can step in and provide them directly through the public sector. But the logical conclusion of this is not to create more money, but to take production out of the market by nationalising the key levers of the economy as part of a rational, democratic, socialist plan.

Ultimately, as long as the economy remains dominated by big business and private monopolies, any money pumped into the system will go to pay for commodities – food and shelter, etc. – that are produced by the capitalists. In other words, all this money will end up in the hands of profiteering parasites.

The aim of the left, therefore, should not be to strengthen the money system, but to abolish it. Implementing MMT’s policy conclusions might end up destroying the value of a currency, but it will not put an end to the power of money. This can only be done by abolishing the system of commodity production and exchange out of which money has historically arisen.

This means tackling the roots of the capitalist system: private ownership and production for profit. Only by bringing in common ownership over the means of production and implementing a socialist economic plan can we satisfy society’s needs. We cannot print our way to socialism.

Capitalism and class

Rather than printing money and bureaucratically managing economic demand, socialists should be calling for economic planning. But you cannot plan what you do not control. And you cannot control what you do not own.

Rather than printing money and bureaucratically managing economic demand, socialists should be calling for economic planning. But you cannot plan what you do not control. And you cannot control what you do not own.

MMT, however, avoids this key question of economic ownership. In fact, it largely avoids the question of capitalist production and the economic laws that govern this altogether. After all, by its own admission, it is not so much an analysis of the capitalist system, but a description of the relationship between government spending, taxes, and the money supply.

In glossing over these questions, however, MMT fails to recognise the fundamental realities of our economy: that it is not just numbers on a screen or equations on a chalkboard, but living flesh and blood, with women and men trying to live their lives and put food on the table.

Indeed, like Keynesianism, MMT’s economic analysis seems completely devoid of the issue of class and the fact that we live in a class society, composed of antagonist economic interests: those of the exploiters, and those of the exploited.

For example, when MMT talks about the state, what kind of state is being referred to? As Marx noted in the Communist Manifesto, under capitalism, “the executive of the modern state is nothing but a committee for managing the common affairs of the whole bourgeoisie”.

If we want a government that will run the economy in the interests of ordinary people, then we need a workers’ state. But where in MMT is the role of the organised working class in running and managing society?

Lenin once remarked that capitalism, far from being a democracy, represented the ‘dictatorship of the banks’. But instead of overthrowing this dictatorship, MMT’s advocates suggest replacing it with another: the dictatorship of one bank – the central bank.

In this future vision of the MMTers, who would be in charge of this omnipotent central bank – the working class or the capitalist class? Similarly with the big monopolies that dominate the economy under capitalism. Are these to remain in private hands, producing for profit?

A national bank, directing society’s resources around the economy, would certainly be a vital element of a socialist plan of production. But in this setup, such a bank would have to be under the control of the working class. Is this what MMT’s supporters envision?

MMTers state that their theory “gives us the power to imagine truly transformational politics”. But, at the end of the day, they do not propose fundamentally challenging the power of the capitalist class, nor altering the current economic relations and the failed dynamics that flow from these. Private property, for them, remains inviolable and sacrosanct. The anarchy of the market is untouched.

Rather than “the working classes seizing the means of production,” prominent MMT theorist Bill Mitchell asserts, “it’s the working classes seizing the means of production of money” (his emphasis). Richard Murphy goes further, reassuring right-wing critics of MMT that its supporters have “no plans to sweep the private sector aside”.

Like their Keynesian predecessors, then, MMTers’ strategy is one that saves and patches up the capitalist system, rather than overthrowing it.

The New Deal

What MMT proposes, therefore, is again nothing but the old Keynesian economics of demand-side management. But such Keynesianism has been tried before – and found wanting.

What MMT proposes, therefore, is again nothing but the old Keynesian economics of demand-side management. But such Keynesianism has been tried before – and found wanting.

This top-down attempt at economic management was in vogue across the advanced capitalist countries throughout the 1960s and 1970s, up until the point where its inflationary policies led to a global capitalist crisis of overproduction, stagflation, and the collapse of the Bretton Woods system that had underpinned the post-war boom.

Today, the call for a Green New Deal (GND) has become popular on the left, advocated by AOC in the US and by left-wing Labour activists in the UK. A key element of the GND proposals put forward on both sides of the Atlantic is the idea of a ‘jobs guarantee’: the provision of a minimum-wage, public sector job to all those who are unemployed.

In this way, left-wing MMTers argue, governments can maintain an ‘appropriate’ level of demand in the economy. Maintaining full employment becomes the primary target. As capitalism’s ‘reserve army of labour’ (as Marx described it) expands and contracts, so too does the government’s own army of labour to compensate.

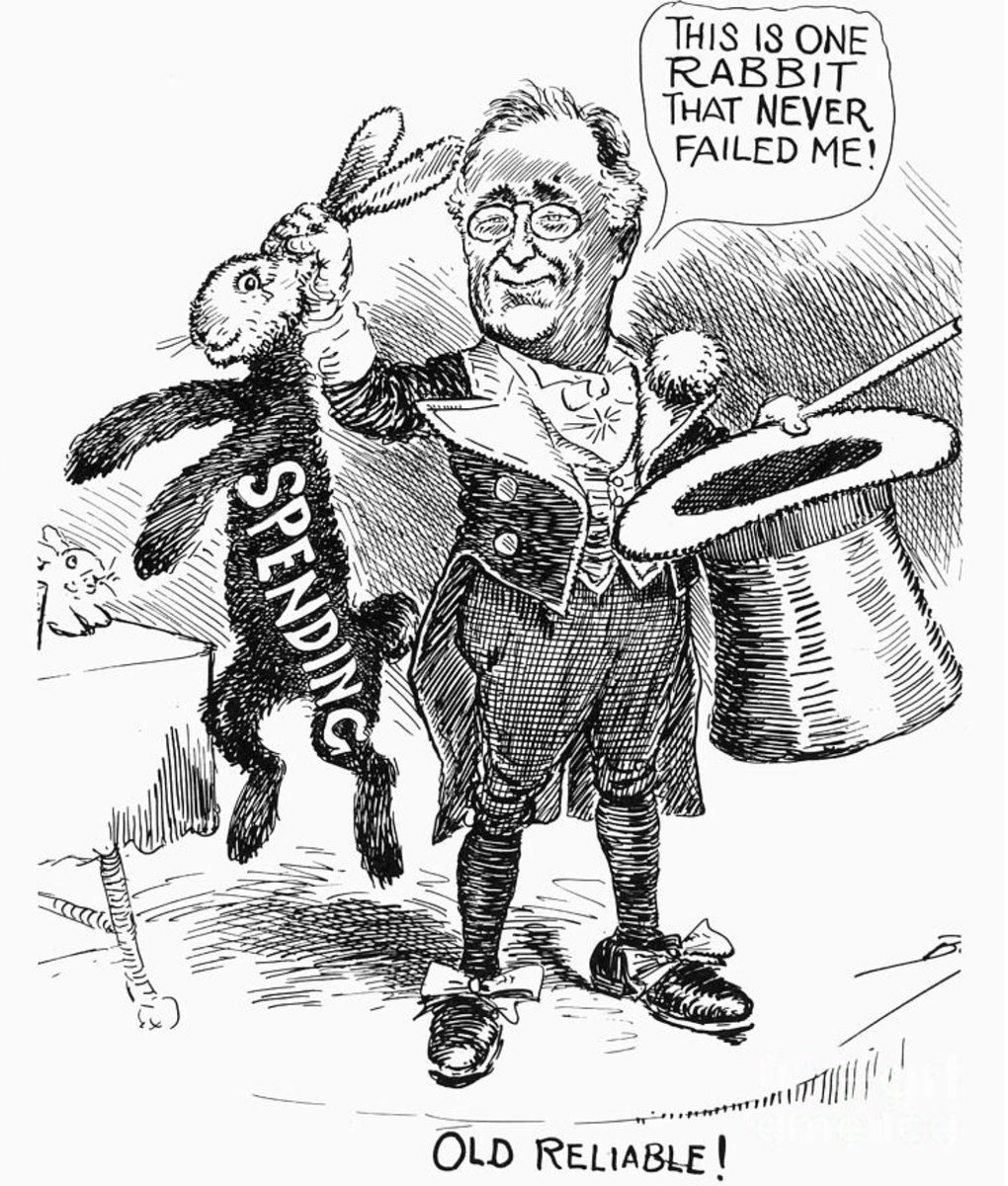

This of course is designed to emulate the original New Deal: President Roosevelt’s programme of public works that were intended to stimulate US economic growth during the Great Depression.

The ideas of Keynes were clearly influential in shaping the New Deal. After all, in his General Theory, the English economist even suggested that the government could boost demand by burying money in the ground and getting workers to dig it back up.

“There need be no more unemployment,” stated Keynes. “It would, indeed, be more sensible to build houses and the like,” he continued, “but if there are political and practical difficulties in the way of this, the above would be better than nothing.”

The only problem that the advocates of a ‘jobs guarantee’ fail to mention, however, is that the New Deal did not work. The slump continued long after its implementation (in fact, it became worse with the rise of ‘beggar-thy-neighbour’ protectionism). Unemployment even went up. Only with the onset of the Second World War and the mopping up of workers into the army and the arms sector did unemployment fall.

Even Keynes himself was forced to admit defeat. “It is, it seems, politically impossible for a capitalistic democracy to organise expenditure on the scale necessary to make the grand experiments which would prove my case — except in war conditions.”

The same can be seen in China today, where the largest ever Keynesian programme of construction has been undertaken in the last decade, in an effort to escape the impact of the global capitalist crisis. But the result has been a massive increase in public debts, on one side, and the ludicrous contradiction of ghost cities alongside a huge housing crisis, on the other.

This is the logical conclusion of Keynesian attempts to bureaucratically manage a capitalist, profit-driven economy. There is no reason to believe a new New Deal would fare any better today in America, Britain, or anywhere else.

And so we arrive back at square one, asking ourselves what MMT really has to offer?

Marxism vs Keynesianism

MMTers, however, are not deterred by the historical failings of similar economic strategies. After all, as MMT advocate Richard Murphy points out in the Financial Times, why should we worry about pushing the economy beyond its productive limits, when “no economy has operated ‘normally’ for more than a decade”.

MMTers, however, are not deterred by the historical failings of similar economic strategies. After all, as MMT advocate Richard Murphy points out in the Financial Times, why should we worry about pushing the economy beyond its productive limits, when “no economy has operated ‘normally’ for more than a decade”.

Indeed, even in times of ‘boom’, the febrile global economy operates far below its productive capacity, only able to limp along thanks to ultra-loose monetary policy and a glut of cheap credit.

‘Excess capacity’ has become a hallmark symptom of a system that has long outlived its usefulness. Even at its height, capitalism can only successfully utilise about 80-90% of is productive abilities (see below). This falls to 70% or less in times of slump. In past recessions, the figure falls to as low as 40-50%.

Across the world today, vast swathes of industry lie idle. Markets are saturated with steel and smartphones. And millions of workers remain unemployed or underemployed.

But the question never asked – either by MMT’s proponents, or those economists of a more traditional Keynesian variety – is how we have ended up in this situation in the first place?

“The use of MMT is akin to pumping up a flat tyre,” remarks Larry Elliott, economics editor of the Guardian. “Once it is fully inflated there is no need to carry on pumping.” But what is the cause of the original puncture?

Why aren’t businesses investing? Why isn’t our full productive capacity being utilised? Why do we see a permanent ‘reserve army of labour’? Why must the government step in to ‘stimulate demand’? Why, in short, is the world economy in a ‘permanent slump’?

To this, the MMTers and Keynesians have no answer. The latter merely state that ‘excess capacity’ is the result of a lack of effective demand. Businesses are not investing because there is not enough demand for the goods they produce. But why?

How has the economy become stuck in this downward spiral of low investment, unemployment, and stagnant demand? And why is this cycle of boom-and-bust (these days, mainly bust) such a never-ending feature of capitalism?

The most that Keynes himself could offer in the way of an explanation was to invoke capitalism’s ‘animal spirits’. The capitalists, he suggested, were simply driven by ‘business confidence’. But this is nothing but philosophical idealism.

Confidence under capitalism has a material basis: the profitability of production. If there are profits to be made, then the capitalists will be brimming with confidence and they will invest. If not, then pessimism – and slump – sets it.

Marxism, by contrast, provides a clear, scientific analysis of the capitalist system, its relations and laws, and why these intrinsically lead to crises. These, in the final analysis, are crises of overproduction. The economy collapses not simply because of a fall in demand (or confidence), but because the productive forces come into conflict with the narrow limits of the market.

Production under capitalism is for profit. But to realise a profit, the capitalists must be able to sell the commodities they produce.

Profit, at the same time, however, is appropriated by the capitalists from the unpaid labour of the working class. Workers produce more value than they receive back in the form of wages. The difference is surplus value, which the capitalist class divides amongst itself in the form of profits, rents, and interest.

The result is that, under capitalism, there is an inherent overproduction in the system. It is not simply a ‘lack of demand’. Workers can never afford to buy back all the commodities that capitalism produces. The ability to produce outstrips the ability of the market to absorb.

Of course, the system can overcome these limits for a time though reinvestment of the surplus into new means of production, or through the use of credit to artificially expand the market. But these are only temporary measures, “paving the way,” in the words of Marx, “for more extensive and more destructive crises” in the future.

The 2008 crash marked the culmination of such a process – a climax that was delayed for decades on the basis of Keynesian policies and a boom in credit alike. But now the crisis has hit, and neither the Keynesians, the MMTers, nor anyone other than the Marxists can explain why.

At most, Keynesianism and MMT provide a palliative medicine for a chronic disease. But neither can diagnose this disease correctly, nor offer a genuine cure.

The point is to change it

MMTers hope that their groundbreaking new outlook can liberate the left, the labour movement, and – in turn – society by giving us the arguments and analytical tools needed to break with the neoliberal consensus, demand the impossible, and achieve our dreams.

MMTers hope that their groundbreaking new outlook can liberate the left, the labour movement, and – in turn – society by giving us the arguments and analytical tools needed to break with the neoliberal consensus, demand the impossible, and achieve our dreams.

But true freedom is not obtained by imagining ourselves to be free of capitalism’s laws. Rather, genuine liberation comes about precisely from understanding these economic laws – and organising to replace them with new ones, based on socialist planning and workers’ control.

The proponents of MMT, in contrast, do not seem interested in scientifically understanding the economy. They imagine that governments can dictate to the market. But under capitalism, it is the market – and the laws of the market – that dictate to governments.

A look at the experience of François Mitterrand’s government in France provides important lessons. Mitterrand was elected in 1981 on the back of a left-wing Keynesian programme, promising nationalisations, a rise in the minimum wage, and a 39-hour week.

But after just two years, facing a flight of capital and a fall in the competitiveness of French industry, the President was forced to undertake a tournant de la rigueur (austerity turn) to fight inflation and regain the confidence of the markets. All of this took place whilst France was a supposedly ‘sovereign’ country.

It is not scaremongering to talk of economic collapse, hyperinflation, capital flight, shortages and sabotage: this is the dire reality faced by workers in Venezuela right now as a result of short-sighted economic policies that are strikingly similar to those proposed by leading figures in the MMT world.

Such ladies and gentlemen may be full of good intentions. But, as the old saying goes, the road to hell is paved with such well-meaning wishes.

As Paul Krugman remarked in regards to mainstream macroeconomic ideas, MMT is not just wrong but harmful – harmful because it sows illusions, preparing the way for disaster and disappointment.

In this respect, we must shout loudly like the little boy in Hans Christian Andersen’s tale – the emperor has no clothes! We have a duty to offer a word of warning to workers and youth: do not believe those trying to foist their quack remedies upon you. Now is not the time for the wiley charms of charlatans and snake-oil salesmen.

We do not criticise MMT from the same position as the apologists of capitalism. No, our criticisms come from a Marxist perspective – from the standpoint of what is good for the world working class; from what is necessary to abolish capitalism and liberate humanity.

The left and the labour movement will not be liberated by carelessly throwing aside the shackles of orthodoxy, but by working out a correct, scientific analysis of the economy. Only in this way can we overthrow the decrepit capitalism system and replace it a socialist plan of production.

This was the task that Karl Marx set himself with his economic writings – in particular, his magnum opus of Capital. In order to change the world, you must first understand it.